Published: 05/07/2024 By Amanda Hunt

Lets look at the main takeaways from the June House Price Index...- House price inflation was flat at 0% in May 2024, but UK house prices are on track to be 1.5% (£3,900) higher by the end of 2024

- UK house prices are currently 8% “overvalued” but will be “fairly valued” by the end of the year due to rising incomes

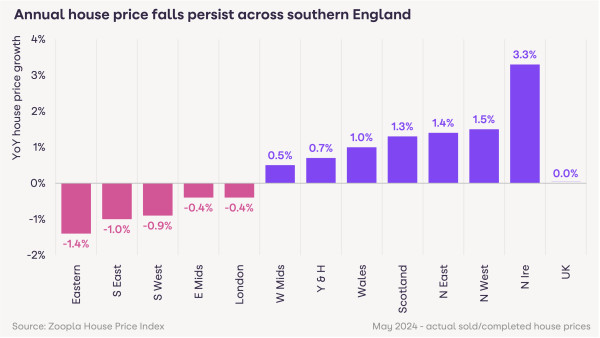

- House prices have risen across all regions over the last 3 months

- Home buyers and sellers largely undeterred by election campaign

- Demand (6%) and sales agreed (8%) are both higher than this time last year

- 75% of the 1.1 million sales projected for this year are either complete or in the sales pipeline

Sales agreed are down slightly month-on-month across all regions, led by the North East (-6%) and West Midlands (-5%). The overall stock of homes for sale continues to grow across all regions, albeit at a slower rate than recorded over recent months. There are still almost a fifth more homes for sale than a year ago.

The annual rate of UK house price inflation is now static at 0% in May 2024, up from a low of -1.3% in November 2023, and +1.6% a year ago. House prices continue to register annual price falls across southern England at a slowing rate. UK house prices are on track to be 1.5% higher at the end of 2024.

Overall, the market has proved resilient, given the rise in mortgage rates. These averaged below 2% in late 2021 and stand at 4.7% today, spiking well over 5% in October 2022 and again over the summer of 2023. Higher borrowing costs have reduced the buying power of new buyers. Rather than sizable price falls, the main impact has been a sharp decline in the number of sales - 23% lower over 2023.

House prices haven’t fallen as there have been few forced sellers. Unemployment has stayed low by historic standards, and there are a relatively small number of people struggling to pay their mortgage - despite wider cost of living pressures.

The recent jump in mortgage rates led to house prices being overvalued by 13% at the end of 2023. This is less severe than in the run up to 2007 (the global financial crisis) and during the “house price bubble” of the late 1980s. Double digit price falls followed both these periods of overvaluation. Price falls have been smaller more recently as the overvaluation was more modest and sales volumes have taken the hit.

It is estimated that house prices were 8% overvalued at the end of March 2024, but by the end of the year this overvaluation will disappear. This assumes house prices rise 1.5% and mortgage rates remain at 4.5%.

Interest rates hold the key. Looking ahead, the short-term outlook for the sales market will depend on the outlook for mortgage rates, which is also dependent on the outlook for interest rates. Any reductions in the base rate over the summer and into the autumn will deliver a boost to market sentiment and sales activity, even though the impact on fixed rate mortgages will likely be more muted.Based on city forecasts for base rates, mortgage rates are expected to remain in the 4-4.5% range.